A Better Way to Define Your ICP

Why customer maturity, not company size, is the foundational input for every major strategic decision your executive team makes

The Contradiction No One Talks About

Calling yourself customer-centric while segmenting customers by headcount is a contradiction. It is also the standard approach.

Microsoft. Slack. Spendesk. Three companies that invested deeply in understanding customers, that built research practices and journey maps and elaborate frameworks for who they were building for. All three organized their market the same way: SMB, mid-market, enterprise. The tiers vary slightly by company. The logic is identical. And it is built on the most primitive measure available: how many people work there.

When I arrived at Spendesk as Chief Product Officer, I found the same model I had seen at every prior stop. Pricing tiers built on headcount bands. ICP documents organized around company size. The sales motion, the product roadmap, the resource allocation: all of it calibrated to employee count. On the surface, this looked like rigor. In practice, it was producing a set of problems that no one could quite diagnose.

We were winning enterprise accounts and watching them churn. We were building features for “enterprise” that almost no one used. We were pricing ourselves out of markets at the low end and undercharging at the high end. The sales team was closing accounts that the product team did not know how to serve. And the product team was building for a “mid-market customer” that turned out not to be a coherent thing.

The problem was not execution. The problem was the map. Company size tells you how many people work somewhere. What it does not tell you is anything about how a customer operates, what they are actually trying to solve, what they already have in place, or what they are ready to adopt. Those are the variables that determine whether a product fits. And they are almost entirely independent of headcount.

That variable is maturity. And once I understood that, it changed everything: product strategy, roadmap, partnerships, growth motion, messaging, and how we allocated capital. Not one of those decisions. All of them.

What Size Gets Wrong

At Spendesk, we had enterprise accounts (companies with thousands of employees) that were managing spend the way a 30-person startup does. One person handling everything. Receipts gathered inconsistently. No policy infrastructure. No system integrations. When we sold them a product built for sophistication, they did not use most of it. When they eventually left for SAP Concur, we told ourselves they had outgrown us. The truth was simpler: we should never have sold to them in the first place. They were not enterprise customers. They were operationally immature customers who happened to have a lot of employees.

We had the reverse problem too. Small companies (under 50 FTEs) that were running their finance function with a sophistication that matched what we expected to see in companies ten times their size. Internal accountants, FP&A resources, ERP integrations, real procurement workflows. We were underserving them and undercharging them. The segmentation model said these were fundamentally different customers. The maturity model said they were the same.

Size had produced the opposite of clarity.

What Maturity Actually Measures

Maturity in any B2B category is not a vague sense of how sophisticated a company is. It is a specific, measurable position on a curve defined by behavioral dimensions. The number of dimensions varies by category. The principle does not.

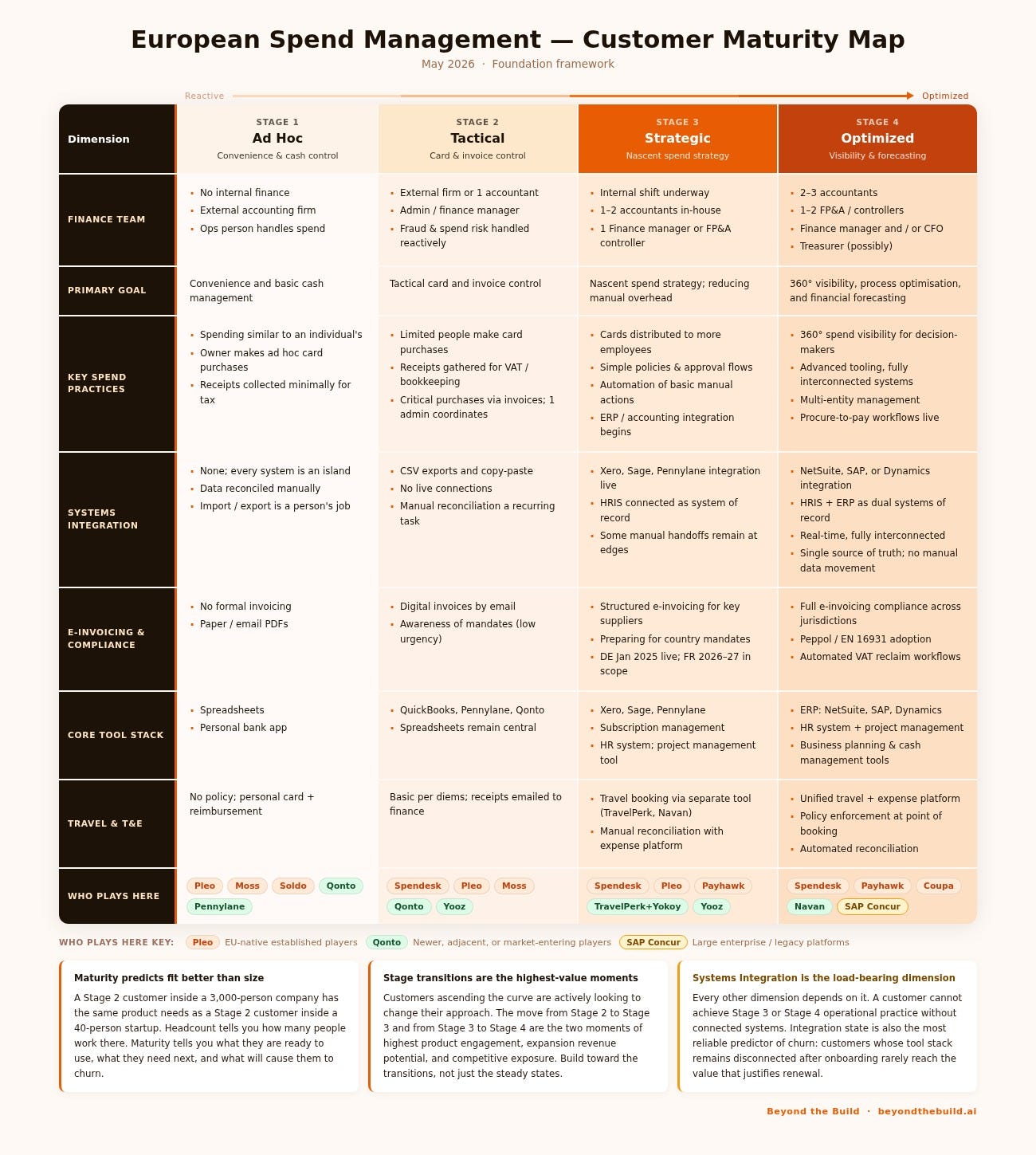

At Spendesk, we decomposed maturity into five dimensions: the composition of the finance team, the primary goal the finance function was trying to achieve, the operating practices around spend, the tool stack in use, and the company’s level of compliance and regulatory engagement. Each dimension was observable. Together, they placed a customer in one of four stages with a precision that headcount never could.

Those stages were Ad Hoc, Tactical, Strategic, and Optimized. Ad Hoc customers were operating reactively: owners making purchases on personal cards, receipts gathered minimally for tax, no internal finance to speak of. Tactical customers had introduced basic control: limited card usage, simple bookkeeping, an external accounting firm or a single accountant. Strategic customers had moved to active management: policies in place, approval workflows, ERP integrations beginning. Optimized customers had achieved systemic control: 360-degree spend visibility, fully interconnected systems, FP&A resources, real-time book closing.

These stages generalize. The specific dimensions change by category, but the underlying progression is consistent across most B2B markets: reactive to managed to systematic to strategic. If you are building any product for any organizational buyer, your customers are somewhere on that curve. The question is whether you have mapped it.

Building the map for your category requires three moves. First, identify the four or five dimensions that most directly determine whether a customer is ready for your product and what they need from it. Not demographics: behaviors, capabilities, and constraints. Second, anchor each stage to a behavioral inflection point: not “companies with 50 to 200 employees” but “a finance function that has shifted from external accounting to an internal hire.” Third, validate the map against your actual customer data. If the stages predict churn, expansion, NPS, and sales cycle length better than your current segmentation does, the map is working.

Four stages is the right number for most categories. That scaffold holds across nearly every B2B market I have encountered.

What the Maturity Model Unlocks

This is where the model becomes more than a categorization tool. A well-constructed customer maturity map is not a better version of an ICP document. It is the foundational input for every major strategic decision the executive team makes. Without it, each of those decisions is being made against an incomplete picture of the market. The consequences compound across the organization in ways that are hard to diagnose precisely because no one is looking at the right variable.

Product strategy.

Size-based segmentation gives the product team a vague brief. “Build for mid-market” is not a product strategy. It is a revenue target dressed up as customer insight, and the product team cannot do much with it beyond guessing at features and working backward from sales requests.

Maturity changes the brief entirely. Once you have mapped your customer base onto the curve, you can answer the questions that actually drive product strategy: which stage holds the highest concentration of customers, where are the biggest capability gaps between what customers have and what they need, and what is the natural next problem for customers ascending the curve?

At Spendesk, this reframing moved us from a strategy organized around “SMB features” and “enterprise features” to one organized around stage transitions. The most valuable product work was not building the most sophisticated features. It was building what unlocked the move from Stage 2 to Stage 3, because that was where our highest customer concentration sat and where the highest expansion value lived. The maturity map made that visible. Headcount data had hidden it entirely.

Product roadmap.

A roadmap without a maturity model tends to accumulate features without coherent direction. Every customer request, every competitive gap, every sales-driven addition gets evaluated on its own merits. The roadmap grows in size without growing in coherence.

The maturity model gives the roadmap a through-line. Every feature can be evaluated against a stage. Does this serve customers in transition from Stage 2 to Stage 3? Does it deepen retention for Stage 4 customers? Is this feature too early, serving sophistication that only a small fraction of customers is ready for? The stage framework does not make every roadmap decision, but it provides a filter that prevents the roadmap from becoming a list of disconnected additions.

It also disciplines scope. When you know which stages you are primarily serving, you know which features are core to those stages and which are distractions. At Spendesk, understanding that our primary sweet spot ran from Stage 2 through Stage 4 made it easier to decline enterprise requirements that would have consumed R&D capacity to serve two accounts rather than thousands. That clarity did not come from a revenue conversation. It came from the map.

Partnership and integration strategy.

This is the domain where the maturity model is most directly operational. The tool stack dimension of the map is essentially an integration roadmap written for you by your customers.

Stage 2 customers are on QuickBooks, Xero, and Sage. If you cannot integrate with those tools, you cannot serve them. Stage 4 customers are on NetSuite, SAP, and Dynamics. If you cannot integrate with those, you will churn them as they ascend. The maturity map tells you exactly which integrations are table stakes at each stage, and therefore which integration investments to prioritize and in what order.

The same logic applies to partnerships. The companies your customers use at each stage are your natural integration partners at that stage and, in some cases, your co-marketing partners or distribution channels. Without the map, partnership strategy tends to be reactive: someone surfaces a referral opportunity, a competitor announces an integration, you respond. With the map, you can sequence partnerships deliberately against the stages you are building toward. The integration roadmap becomes a strategic document, not a backlog of requests.

Product-led growth strategy.

PLG is not a single motion. It is a set of motions that work differently depending on where a customer sits on the maturity curve. Applying a uniform PLG strategy to customers at different stages is one of the most common reasons PLG efforts underperform.

Stage 1 and 2 customers respond to simplicity and low-friction activation. The product is the salesperson. Self-serve works because the decision is low-stakes, the value is immediate, and there is no complex integration or change management to navigate. Stage 3 and 4 customers have a different buying dynamic. There are more stakeholders, more existing infrastructure to integrate with, and more organizational inertia to overcome. A self-serve motion that works at Stage 2 stalls at Stage 4 without a sales assist at the right moment in the activation flow.

The maturity model tells you where self-serve can carry the full motion and where it has to hand off. It also tells you where the natural expansion triggers live: what a Stage 2 customer does inside the product that signals they are ready for the Stage 3 conversation, and how to surface that signal in the product experience. Early-stage customers are a PLG motion: low friction, self-serve, product does the selling. Mid-stage customers are a PLS motion: product-led sales, where the product creates the opening and a human closes it. Late-stage customers are an SLG motion: sales-led from the start, with the product doing proof rather than acquisition. Without the map, companies apply one of these motions to all three audiences, and wonder why conversion looks inconsistent.

Positioning and messaging.

A Stage 2 finance team inside a 50-person startup and a Stage 2 finance function inside a 3,000-person company have the same problem. If your messaging speaks to company size, it reaches neither of them well. The startup assumes the product is not for them. The large company assumes they are already past it. If your messaging speaks to their stage (”if your team is still closing the books manually at month-end”) it speaks directly to both, regardless of how many people work there.

This is the positioning implication that most companies miss. Maturity-stage messaging is more precise and reaches a wider audience simultaneously. It also clarifies who you are competing against at each stage, which changes the differentiation story. At Stage 2, the competitor is often a spreadsheet or a basic accounting tool. At Stage 4, it is SAP Concur. The evidence you need to provide, the objections you need to address, the language that builds credibility: all of it is different. A single positioning that tries to speak to all stages at once tends to speak persuasively to none of them.

The maturity model makes it possible to build positioning that is coherent at each stage and sequenced across them, so that customers who find you at Stage 2 can grow into Stage 4 without ever feeling like they have moved beyond what you stand for.

Resource allocation and unit economics.

This is where the maturity model reaches the CFO and the board. And it is where the failure to build it tends to be most expensive.

If R&D investment is being allocated toward enterprise features because larger companies mean larger deals and better unit economics, but your actual enterprise accounts are Stage 2 customers who churn because they were oversold, the investment thesis is wrong. The capital is going toward the wrong customer segment. The sales team is celebrating logos that will not renew. The financial model is projecting revenue from accounts that will not stay.

LTV to CAC ratios vary by stage, not by size. Stage 3 and 4 customers who are well-served tend to expand, refer, and stay for years. Stage 2 customers who were sold more product than they were ready for tend to underuse, disengage, and churn. The difference in unit economics is large, and it shows up clearly in cohort data once you have the maturity framework to read it against. Before that, it tends to look like a retention problem or a customer success resourcing issue. It is neither. It is a customer fit problem that originates in the segmentation model.

Pricing architecture follows the same logic. Pricing aligned to headcount bands is an approximation of willingness to pay that tends to be wrong in both directions. Pricing aligned to stage transitions prices against the value that actually drives the customer’s decision to buy and to expand. Moving toward stage-informed pricing at Spendesk made the commercial model more coherent and surfaced expansion revenue the prior model had structurally obscured.

What AI changes, and what it doesn’t

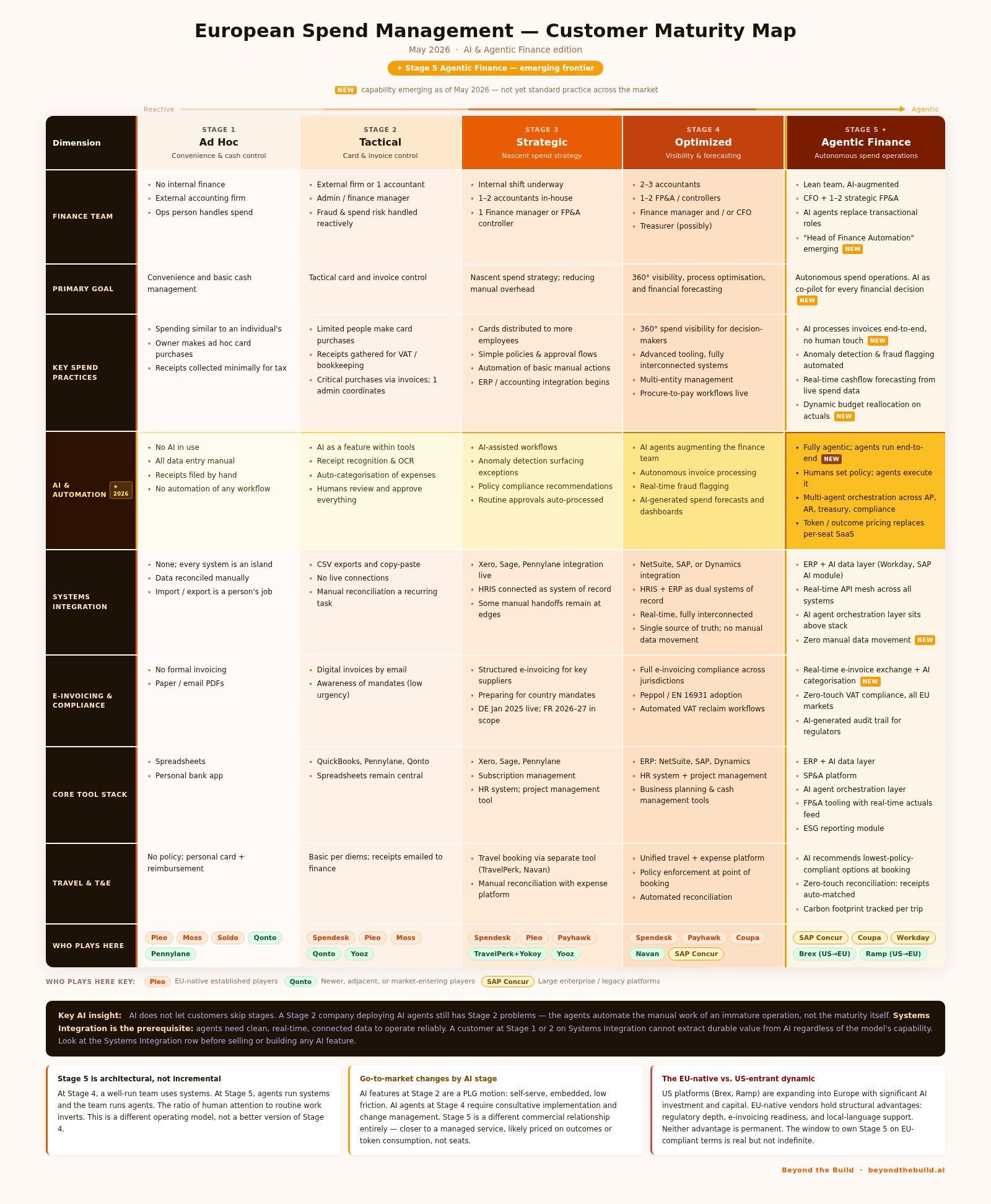

The maturity model now has a sixth dimension worth mapping in every B2B category: AI and automation readiness. And in most markets, a fifth stage is becoming visible.

That fifth stage is not an incremental improvement on Stage 4. The move from Optimized to what I would call Agentic is architectural. At Stage 4, a well-run team uses systems. At Stage 5, agents run systems and the team runs agents. The ratio of human attention to routine work inverts. The cost structure changes. The skills required to manage the function change. It is not more of Stage 4. It is a different operating model.

Adding AI and automation as a dimension does something specific: it makes visible a gap that most companies are currently hiding from themselves. A company’s operational maturity and its AI maturity do not move in parallel. A Stage 3 operation can be at Stage 1 on AI adoption. A Stage 4 team can be running on Stage 2 tooling with no meaningful automation. That gap is a product insight, a sales insight, and a risk signal all at once.

It is also where the most consequential mistake of the current AI moment lives. AI does not let customers skip stages. A Stage 2 company deploying AI agents still has Stage 2 problems. The agents automate the manual work of an immature operation, not the maturity itself. The demos will look impressive. The retention numbers will not.

Which brings the dependency into focus. Systems Integration is the prerequisite for meaningful AI deployment, not a parallel track. Agents need clean, connected, real-time data to operate reliably. A customer at Stage 1 or 2 on systems integration cannot extract durable value from AI agents regardless of how capable the underlying model is. The accuracy and trust problems compound directly when the data pipeline beneath the AI is broken or manual. The maturity map tells you something important about AI readiness before you build or sell a single AI feature: look at the systems integration row first.

The go-to-market logic follows the same stage-based structure as everything else. AI features embedded in existing workflows at Stage 2 are a PLG motion: self-serve, low-friction, product does the selling. AI agents at Stage 4 require a consultative implementation motion, change management, and a longer sales cycle. Stage 5 is a different commercial relationship entirely. Not a SaaS subscription but a managed service, with pricing logic that shifts from seats to outcomes or consumption. (See, Why AI is Breaking your SaaS Pricing Model.)

For CEOs and CPOs, the practical question is not how to add AI to the product. It is at which stage AI creates durable value for customers, and what the maturity map says about how many of them are actually there.

The Map Changes the Question

Product strategy, roadmap, partnerships, growth motion, messaging, capital allocation. Every one of those decisions is downstream of how you define your customer. A wrong definition does not produce one bad decision. It produces all of them, compounded.

The maturity model does not improve the answer. It replaces the question.

One question produces a data point. The other produces a strategy.